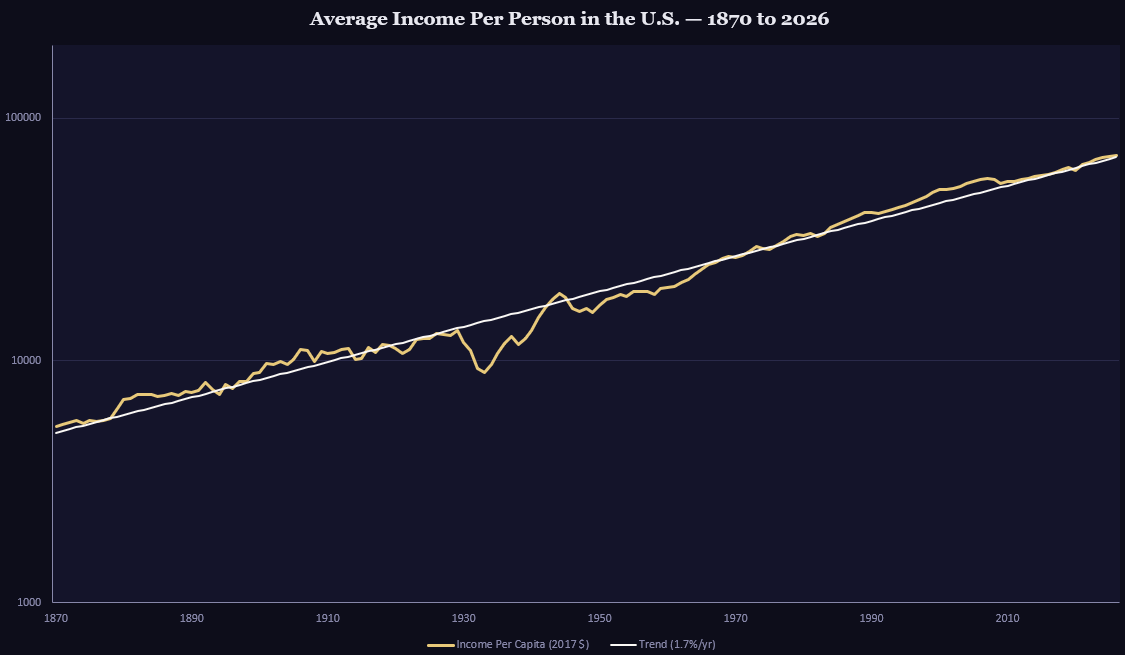

A few weeks ago I watched a lecture by Chad Jones, an economist at Stanford, on AI and long-run economic growth. He opened with a simple chart: US income per person since 1870, plotted on a log scale. A straight line. Around 2 percent annual growth for 150 years.[1]

That line is remarkable because of what it hides. Railroads. Electricity. The internal combustion engine. Semiconductors. The internet. Each one was supposed to change everything. And each one, eventually, did. But the aggregate growth rate barely moved. The line stayed straight.

How is that? One thought is the counterfactual: without those innovations, income would have stagnated. The 2% line wasn't the ceiling; it was the floor. Each technology prevented the plateau that would have come without it.

That reframe matters. If prior technologies merely kept us at 2% rather than lifting us above it, the right question isn't whether AI continues the trend. It's whether AI is the first technology capable of bending it.

If the counterfactual view is right, AI simply allows the 2% to continue. That's the bear case, and it deserves respect. It draws on a serious observation: past technologies took decades to move the needle on aggregate productivity. Railroads required laying track. Electricity required wiring an entire nation. The physical constraints of deployment smoothed the impact across decades and blended it into the long-run trend.

My base case is different, and the distinction is structural. AI is software. It deploys across existing networks at near-zero marginal cost, without waiting for a grid to be built or a right-of-way to be cleared. The constraint isn't infrastructure; it's adoption. And adoption curves for software are not linear.

This compression is the key variable. Consider what happened to communication when email replaced postal mail. The productivity gain wasn't new; faster decisions and lower coordination costs had always been valuable. What changed was the speed of delivery. The same output arrived in seconds instead of days, and the economic impact landed in years rather than decades. AI is that dynamic applied to cognitive work broadly: the same gains that would have taken a generation to accumulate arrive inside a single business cycle. The numerator stays the same; the denominator shrinks. Growth spikes. That's not a forecast; it's math.

Prior automation was largely physical: machines replaced muscle. AI replaces the cognitive steps that sit upstream of nearly every economic activity, research, planning, analysis, communication. When you compress the cost of thinking, the deflationary pressure isn't confined to a sector. It's embedded in the production function of the entire economy.

The skeptic's objection is the law of large numbers. The US economy is enormous. The 2% gravitational pull is real and powerful. I take that seriously. But the objection assumes that AI's adoption curve resembles the infrastructure buildouts of the past. It doesn't. The distribution mechanism already exists. The bottleneck is training, inference cost, and organizational adoption, all of which are compressing faster than the models assume.

There are risks to this view. Regulatory constraints, energy supply, or unexpected technical limits could slow deployment and pull the timeline back toward the historical pattern. Data centers and power generation are real physical constraints.

But consider what that means. If deployment slows, AI looks like every prior technology: a 2% outcome. If deployment proceeds at anything close to current rates, the growth impact is front-loaded in a way that has no modern precedent.

The 2% trend line is a rearview mirror. It reflects the physics of past industrial revolutions, the time it takes to wire a nation or lay a thousand miles of track. AI doesn't have those physics. The line doesn't have to stay straight, and I think it won't. But the economy and markets run on different clocks. The economy will take years to register a structural break. Markets price it in the afternoon. That gap is where valuation risk lives. I'm a bull on the curve. I'm more cautious on what you're paying to own it today.

IMPORTANT DISCLOSURES

Zidle Macro Strategy Group is an independent macroeconomic research and commentary service. The content in this publication is informational and analytical in nature and does not constitute investment advice, a solicitation, or an offer to buy or sell any security or investment product. ZidleMSG is not a registered investment adviser, broker-dealer, or fiduciary under any federal or state securities law.

This publication does not recommend, endorse, or make any specific buy, sell, or hold recommendation for any security, ETF, mutual fund, private fund, or other investment vehicle. Any companies, individuals, or projects referenced are discussed solely for analytical and illustrative purposes. ZidleMSG has no financial relationship with, and receives no compensation from, any entity mentioned in this publication.

All commentary represents the views of the author based on publicly available information and macroeconomic analysis. Such views are subject to change without notice. Past commentary does not constitute a performance track record, and no representation is made that any analysis or forward-looking view will prove accurate.

Investing involves risk, including the possible loss of principal. Readers should conduct their own independent research and consult a qualified financial, legal, or tax professional before making any investment decision. ZidleMSG assumes no liability for any investment decisions made in reliance on this content.

© Zidle Macro Strategy Group. All rights reserved. Reproduction or redistribution of this content, in whole or in part, is prohibited without the prior written permission of ZidleMSG.

[1] https://web.stanford.edu/~chadj/AIandEconomicFuture.pdf