I had a conversation recently with a longtime friend, one of the sharpest investors I know. We talked about what's really happening to the generation entering the workforce for the first time, and whether the people who can't find traditional jobs are the same people starting companies at a record pace.

That conversation has stayed with me.

Entry-level hiring has contracted sharply as companies automate intake tasks and compress headcount at the bottom of the org chart. The standard narrative is straightforward: AI is displacing young workers, and that's a problem.

Here's what the standard narrative misses.

The Formation Data

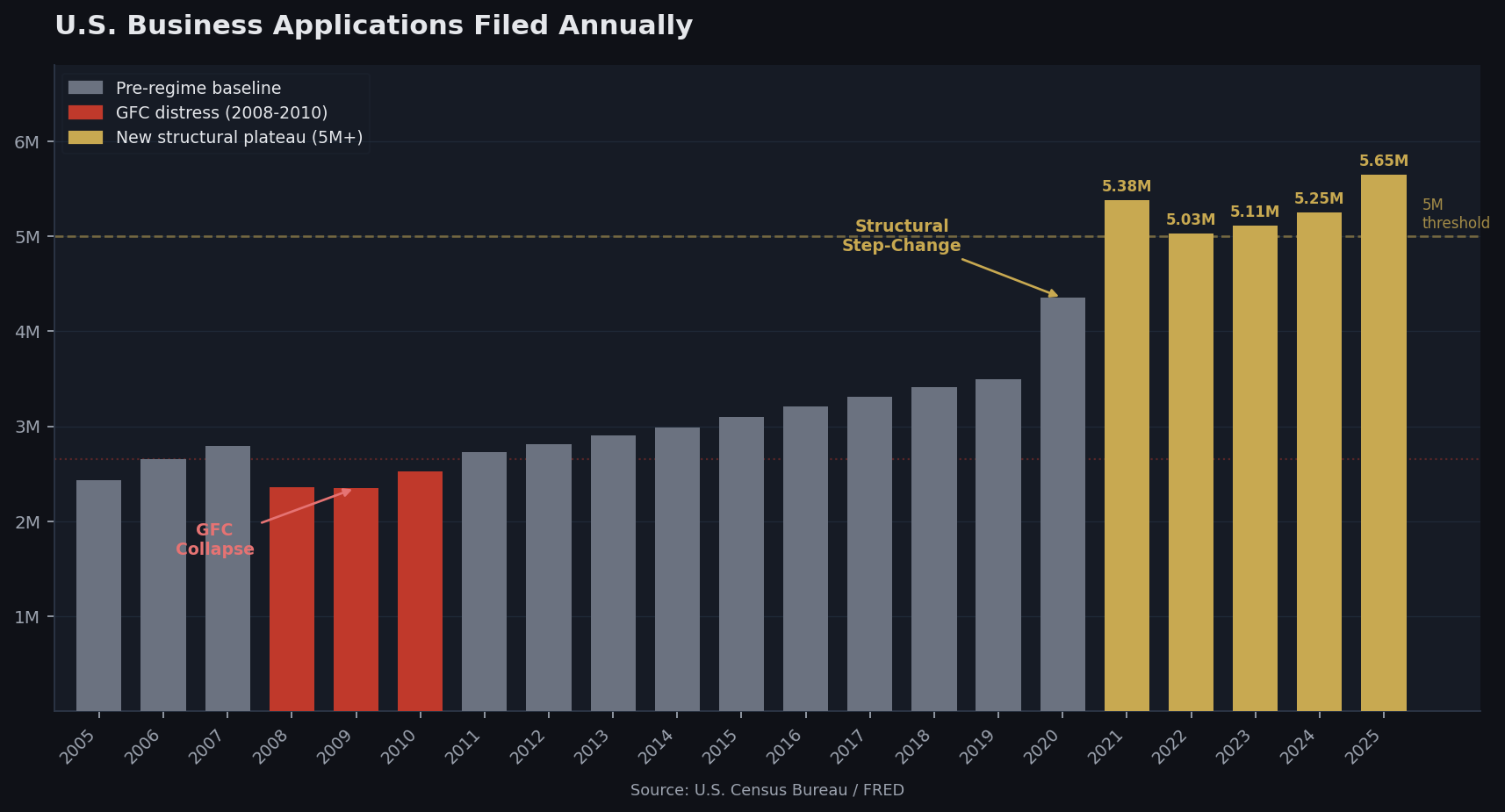

In 2025, approximately 5.65 million new business applications were filed in the United States, per FRED. That is roughly 8% above 2024's total of 5.25 million, and it represents the fourth consecutive year above 5 million, a structural level the country had never reached before 2020.

To understand why this matters, consider what the same data looked like during the last period of elevated economic stress. In 2007, business formation totaled 2.65 million applications. In 2008, it fell. In 2009, it fell further, reaching near-series lows. In 2010, it had not recovered. The 2008 analogy is not supported by the data. The argument that rising youth unemployment combined with elevated business formation signals a "distress pattern" collapses on contact with history: during actual distress, formation collapsed. What we are seeing today is not a distress spike. It is a sustained structural step-change that has persisted through an expansion. Those are different animals.

Y Combinator's (the premier Silicon Valley startup accelerator) 2025 batch was its largest in history, with AI-native companies representing the majority of funded startups. One data point. But it rhymes with the formation numbers, and that's hard to dismiss.

The Proxy That Matters Most

The strongest argument for what is actually happening sits in the official productivity data.

Nonfarm Business Labor Productivity averaged approximately +0.9% annual growth from 2011 through 2019. That was the stagnation era, a decade of flat productivity that confounded economists and suppressed real wages across the income distribution.

Then:

- 2023: +2.3%

- 2024: +3.3%, the strongest reading since the post-recession bounce of 2009-2010

- 2025: +2.6%

That is not noise. That is 2-3x the pace of the prior decade, sustained across multiple years, showing up in official government data. The productivity acceleration that general purpose technology adoption historically produces, documented through electrification and the computing revolution, is measurable. It is already in the numbers.

This is the falsifiable proxy. When critics argue that AI's economic impact is "digital dark matter," present in theory but absent in measurement, the answer is on the FRED website. Pull the series. Look at the chart.

The Honest Counterargument

The bearish case deserves respect. Business formation data captures applications, not survivorship. Most of these ventures will fail. Youth unemployment is real hardship for real people, not an abstraction. And productivity gains at the aggregate level can coexist with severe distributional damage at the individual level.

All of that is true. None of it changes the structural read.

The question for investors is not whether every new business application becomes a going concern. The question is whether the underlying conditions (low barrier formation, AI-enabled leverage for small operators, a generation of founders who cannot get hired so they hire themselves) are consistent with an economy in the early stages of a productivity regime change. The data says yes.

Investment Implication

Position for the productivity regime, not the unemployment headline. The formation data and the productivity data are telling the same story from different angles. Elevated business formation at scale is an input into future economic dynamism. Productivity running at 2-3x its decade average is an output that is already registering.

The generation that cannot find traditional employment is not dropping out. It is forming companies. History suggests that is how regime changes begin, not with a press release, but with talented people who ran out of other options and built something instead.

That is the trade. Stay with it.

IMPORTANT DISCLOSURES

Zidle Macro Strategy Group is an independent macroeconomic research and commentary service. The content in this publication is informational and analytical in nature and does not constitute investment advice, a solicitation, or an offer to buy or sell any security or investment product. ZidleMSG is not a registered investment adviser, broker-dealer, or fiduciary under any federal or state securities law.

This publication does not recommend, endorse, or make any specific buy, sell, or hold recommendation for any security, ETF, mutual fund, private fund, or other investment vehicle. Any companies, individuals, or projects referenced are discussed solely for analytical and illustrative purposes. ZidleMSG has no financial relationship with, and receives no compensation from, any entity mentioned in this publication.

All commentary represents the views of the author based on publicly available information and macroeconomic analysis. Such views are subject to change without notice. Past commentary does not constitute a performance track record, and no representation is made that any analysis or forward-looking view will prove accurate.

Investing involves risk, including the possible loss of principal. Readers should conduct their own independent research and consult a qualified financial, legal, or tax professional before making any investment decision. ZidleMSG assumes no liability for any investment decisions made in reliance on this content.

© Zidle Macro Strategy Group. All rights reserved. Reproduction or redistribution of this content, in whole or in part, is prohibited without the prior written permission of ZidleMSG.