Why the Next Leg of the AI Trade Goes to the Adopters

History has a consistent verdict on infrastructure booms: the builders create the conditions, and the adopters capture the gains.

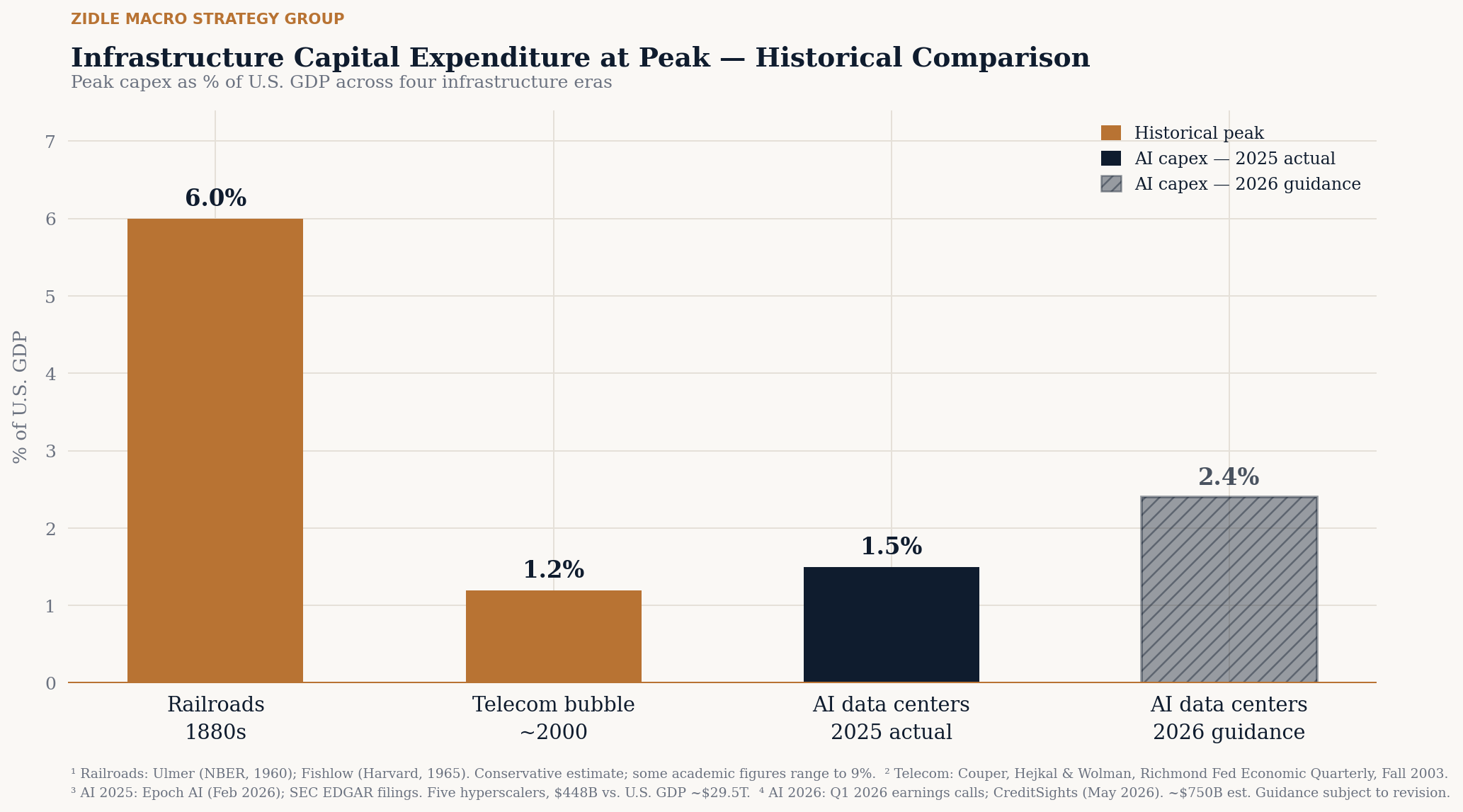

The railroad boom of the 1880s saw U.S. capital expenditure peak at 6% of GDP. The returns came. Every dollar spent on building or expanding railroads grew the economy by $4.20 (in GDP growth) between 1828 and 1860. Plenty of railroads went bankrupt. The infrastructure transformed the economy. The lasting wave of value creation went not to the rail companies but to the industries that reorganized around what they made possible.

Samuel Insull built the largest private electricity empire in American history, spanning 32 states by 1930. He went bankrupt in 1932. The grid survived and grew. The winners were Ford and the manufacturers who redesigned their factories entirely around cheap electricity. The productivity explosion of the 1920s went not to the infrastructure owners but to the companies that built their operations around the power.

Telecom capital expenditure peaked at approximately 1.2% of GDP at the height of the internet buildout. WorldCom and Global Crossing borrowed billions to lay fiber. When the cycle cleared, the infrastructure did not go to waste. Amazon, Google, and Netflix were built on what remained. The infrastructure became indispensable. The next wave of compounding went to the companies that built businesses around it.

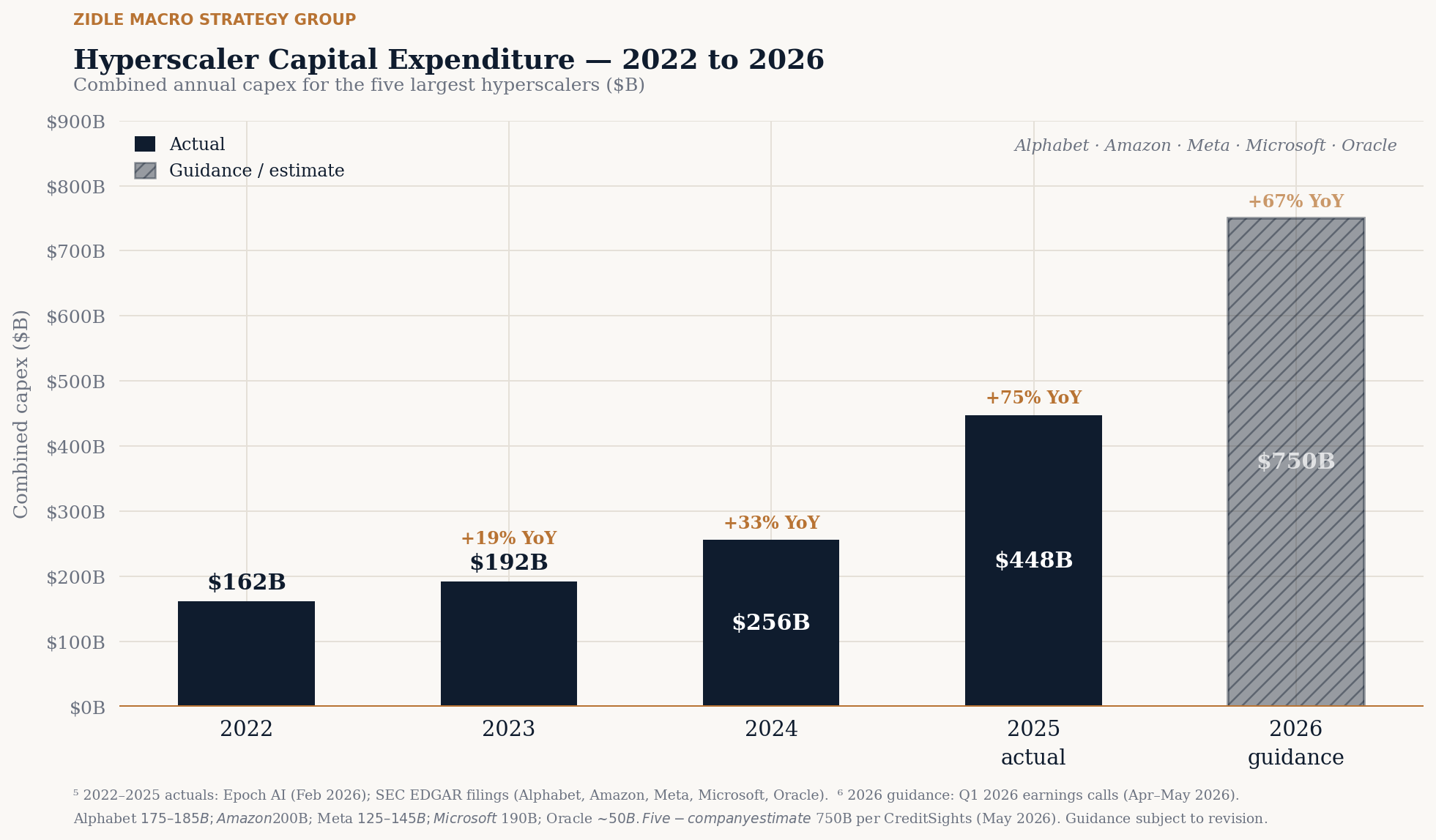

The current AI buildout fits the same pattern. AI data center capital expenditure in 2025 came in at approximately 1.5% of U.S. GDP, with 2026 guidance pointing to 2.4%. The five largest hyperscalers deployed $448 billion in 2025, up 75% from $256 billion the prior year, with combined 2026 guidance now exceeding $750 billion. This is not reckless speculation. It is how transformative infrastructure gets built.

And the hyperscalers executing this buildout are stronger than any infrastructure builder in history. The railroads were single-purpose companies funded by bond markets and land grants. The telecom companies were leveraged to the hilt on borrowed money. Microsoft, Alphabet, Amazon, and Meta are diversified, cash-generating platform businesses funding this buildout from free cash flow. They have already been well-rewarded for Phase 1. The question is where the next return comes from.

The pattern across every major infrastructure cycle is the same. Phase 1 creates the foundation. Phase 2 belongs to the companies that figure out how to build on it.

U.S. labor productivity in the AI era is running at 2.5 percentage points annualized, more than double the pre-pandemic baseline. Finance, manufacturing, and healthcare are leading the adoption curve. The Phase 2 opportunity is not theoretical; it is already emerging. The companies pulling away from the field are rewiring their underwriting models, rebuilding their drug discovery pipelines, restructuring their supply chain logic around intelligence as a cheap, continuously improving input. The gap between operational leaders and laggards will compound over the next 12 to 36 months as the productivity pickup broadens across the economy.

This is where the next wave of durable value creation sits: companies with pricing power, sticky customer relationships, and evidence of genuine workflow redesign rather than AI-as-feature deployment. The infrastructure they are building on is real, well-funded, and becoming more capable every quarter. The substrate is in place.

Phase 1 rewarded exposure. Phase 2 rewards discernment. The companies that pull away from the field will be led by managements that treat AI the way Ford treated electricity: not as a feature to add, but as a foundation to build around. Separating those companies from the ones that do not is where the alpha lives.

Samuel Insull built the grid. Ford built the future.

IMPORTANT DISCLOSURES

Zidle Macro Strategy Group is an independent macroeconomic research and commentary service. The content in this publication is informational and analytical in nature and does not constitute investment advice, a solicitation, or an offer to buy or sell any security or investment product. ZidleMSG is not a registered investment adviser, broker-dealer, or fiduciary under any federal or state securities law.

This publication does not recommend, endorse, or make any specific buy, sell, or hold recommendation for any security, ETF, mutual fund, private fund, or other investment vehicle. Any companies, individuals, or projects referenced are discussed solely for analytical and illustrative purposes. ZidleMSG has no financial relationship with, and receives no compensation from, any entity mentioned in this publication.

All commentary represents the views of the author based on publicly available information and macroeconomic analysis. Such views are subject to change without notice. Past commentary does not constitute a performance track record, and no representation is made that any analysis or forward-looking view will prove accurate.

Investing involves risk, including the possible loss of principal. Readers should conduct their own independent research and consult a qualified financial, legal, or tax professional before making any investment decision. ZidleMSG assumes no liability for any investment decisions made in reliance on this content.

© Zidle Macro Strategy Group. All rights reserved. Reproduction or redistribution of this content, in whole or in part, is prohibited without the prior written permission of ZidleMSG.

Footnotes:

Railroad peak capex: Melville J. Ulmer, Capital in Transportation, Communications, and Public Utilities: Its Formation and Financing (Princeton University Press for NBER, 1960); Albert Fishlow, American Railroads and the Transformation of the Ante-Bellum Economy (Harvard University Press, 1965).

Federal Reserve Bank of Richmond Economic Quarterly, SEC EDGAR 10-K and 10-Q filings