The last couple of weeks were a reminder of something the market learned painfully in 2022 and seems determined to relearn on a rotating basis: the stock-bond relationship is not as reliable as you think.

Between May 14 and May 19, the 10-year Treasury yield surged 20 basis points to 4.67%. The S&P 500 shed roughly 150 points. Not a crash, but a sharp enough jolt to make the point. When rates move up with conviction, stocks and bonds fall together, and the foundational logic of the traditional 60/40 portfolio quietly breaks down.

This is not a new observation. But knowing something and actually feeling it in a portfolio are two different things.

How We Got Complacent

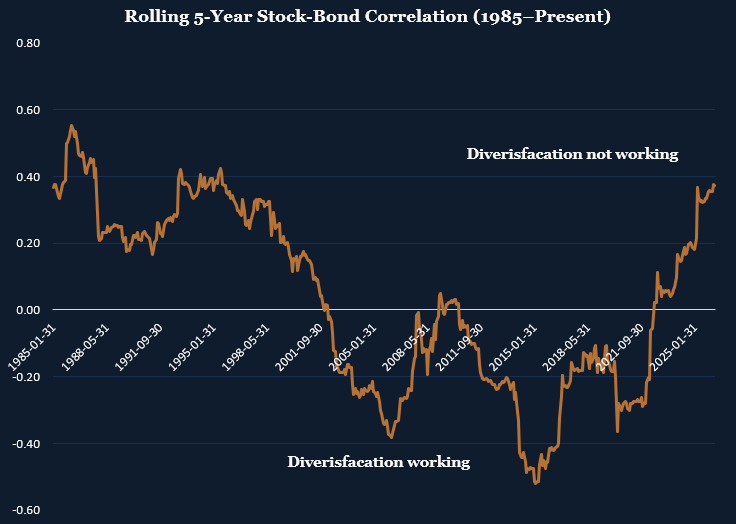

Go back to the 1980s and 1990s, and the stock-bond correlation was solidly positive, averaging around 0.34 in the 1980s and 0.30 in the 1990s. Stocks and bonds tended to move in the same direction. Diversification, in the modern sense, was not really the point; growth was the point, and everything went up together as inflation fell, rates declined, and the economy expanded through two decades of broadly favorable conditions.

The shift happened in the early 2000s. The correlation turned negative, bottoming at around -0.52 in 2015 and averaging -0.24 through the 2010s. For the better part of two decades, when stocks fell, bonds rallied. The 60/40 worked beautifully. Rebalancing felt automatic. Risk management felt elegant. A generation of investors and advisors built their practices around a relationship that, in historical context, was actually the exception, not the rule.

That is the complacency. We mistook a 20-year regime for a natural law.

2022 Was the Wake-Up Call...

In 2022, the Fed moved faster than it had in decades. Inflation was running hot, and the Fed had fallen behind. When it finally acted, it acted hard. The result was something most modern portfolios were not built to handle: stocks and bonds fell simultaneously. The S&P 500 dropped roughly 18%. The Bloomberg Aggregate Bond Index fell over 13%. A classic 60/40 portfolio had one of its worst years in modern history, and diversification offered no shelter.

The correlation flipped positive, and the cushion disappeared.

The 2020s as a whole tell the story in the data. The average rolling correlation has been approximately 0.015 this decade, effectively zero, swinging from -0.36 to as high as +0.37. The old regime of reliable negative correlation is gone. What replaced it is not a new regime so much as an unstable one.

It Is Happening Again

The rolling 5-year correlation as of April 2026 sits at approximately 0.37, near the top of its recent range and firmly in positive territory. That means stocks and bonds are moving in the same direction more often than not. The hedge you think you have is not doing what you think it is doing.

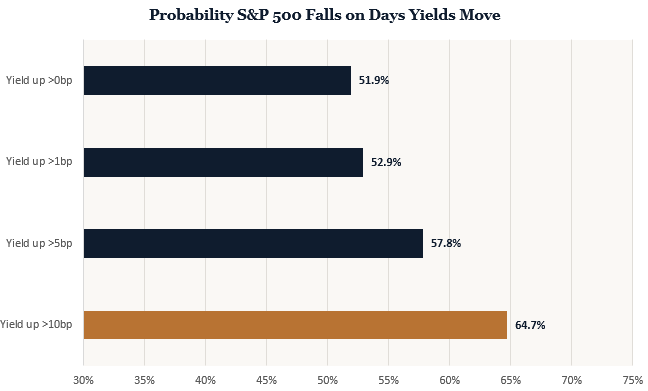

The numbers bear this out at a shorter time horizon too. Looking at daily data since January 2022, on days when the 10-year yield rises more than 10 basis points, the S&P 500 falls about two-thirds of the time. Treasuries are an effective hedge when stock prices fall. When bond yields rise and bond prices fall, equities are not returning the favor. The protection runs one way.

Why This Is Not Going Away

The 20-year stretch of reliable negative correlation was built on a specific set of conditions: falling inflation, declining rates, and a Fed that could cut aggressively whenever growth stumbled. Every time the economy softened, the playbook worked. Bonds rallied, stocks recovered, and the 60/40 looked smart.

Those conditions are no longer in place. The Fed is holding at 3.50–3.75%, and I expect the next move to be a hike before year end, possibly two. Inflation has not been decisively beaten. Treasury issuance is a structural headwind that keeps upward pressure on the long end of the curve regardless of what the Fed does at the short end. The 10-year at 4.67% is not pricing a booming economy; it is pricing term premium and fiscal risk.

What To Do About It

Prepare for more volatility in the stock / bond correlation. The rolling data shows it does oscillate.

A portfolio built around a static 60/40 and left on autopilot is more exposed than it looks. Bonds are only defensive when the correlation cooperates. Cash and short-dated Treasuries sidestep the duration risk entirely. Strategies that are genuinely uncorrelated to both equities and rates, macro, trend-following, real assets, deserve a real allocation, not a token one. Active duration management is not exotic anymore. It is basic risk management for the environment we are actually in.

The stock-bond relationship was reliable for a long time. It may be again someday. But the investors who do best from here will be the ones who stopped pretending it is reliable now.

IMPORTANT DISCLOSURES

Zidle Macro Strategy Group is an independent macroeconomic research and commentary service. The content in this publication is informational and analytical in nature and does not constitute investment advice, a solicitation, or an offer to buy or sell any security or investment product. ZidleMSG is not a registered investment adviser, broker-dealer, or fiduciary under any federal or state securities law.

This publication does not recommend, endorse, or make any specific buy, sell, or hold recommendation for any security, ETF, mutual fund, private fund, or other investment vehicle. Any companies, individuals, or projects referenced are discussed solely for analytical and illustrative purposes. ZidleMSG has no financial relationship with, and receives no compensation from, any entity mentioned in this publication.

All commentary represents the views of the author based on publicly available information and macroeconomic analysis. Such views are subject to change without notice. Past commentary does not constitute a performance track record, and no representation is made that any analysis or forward-looking view will prove accurate.

Investing involves risk, including the possible loss of principal. Readers should conduct their own independent research and consult a qualified financial, legal, or tax professional before making any investment decision. ZidleMSG assumes no liability for any investment decisions made in reliance on this content.

© Zidle Macro Strategy Group. All rights reserved. Reproduction or redistribution of this content, in whole or in part, is prohibited without the prior written permission of ZidleMSG.