I picked up Saturday's Wall Street Journal with my morning coffee, and the front page told me everything I need to know about where we are. On the top, we had a story about how Americans are keeping their cars for nearly 13 years on average because high vehicle prices have shut them out of the new car market. At the bottom of the page, there was an article about restaurants charging $40 for half a rotisserie chicken. These two stories are not contradictions. They are the perfect map of our K-shaped economy.

May CPI drops tomorrow. Whatever it shows, the trend is clear: inflation has been firming all year, jumping to 3.8% in April from 3.3% in March. This accelerating inflation is hammering the average consumer. The University of Michigan Consumer Sentiment Index plunged to 49.8 in April, down from 53.3 in March. That is the lowest reading on record, below levels last seen at the worst of the 2022 inflation shock.

Yet the broader economy is growing. First quarter GDP grew at a 1.6% annualized rate. The stock market has set 23 record highs in 2026 alone, with the S&P 500 near 7,400.

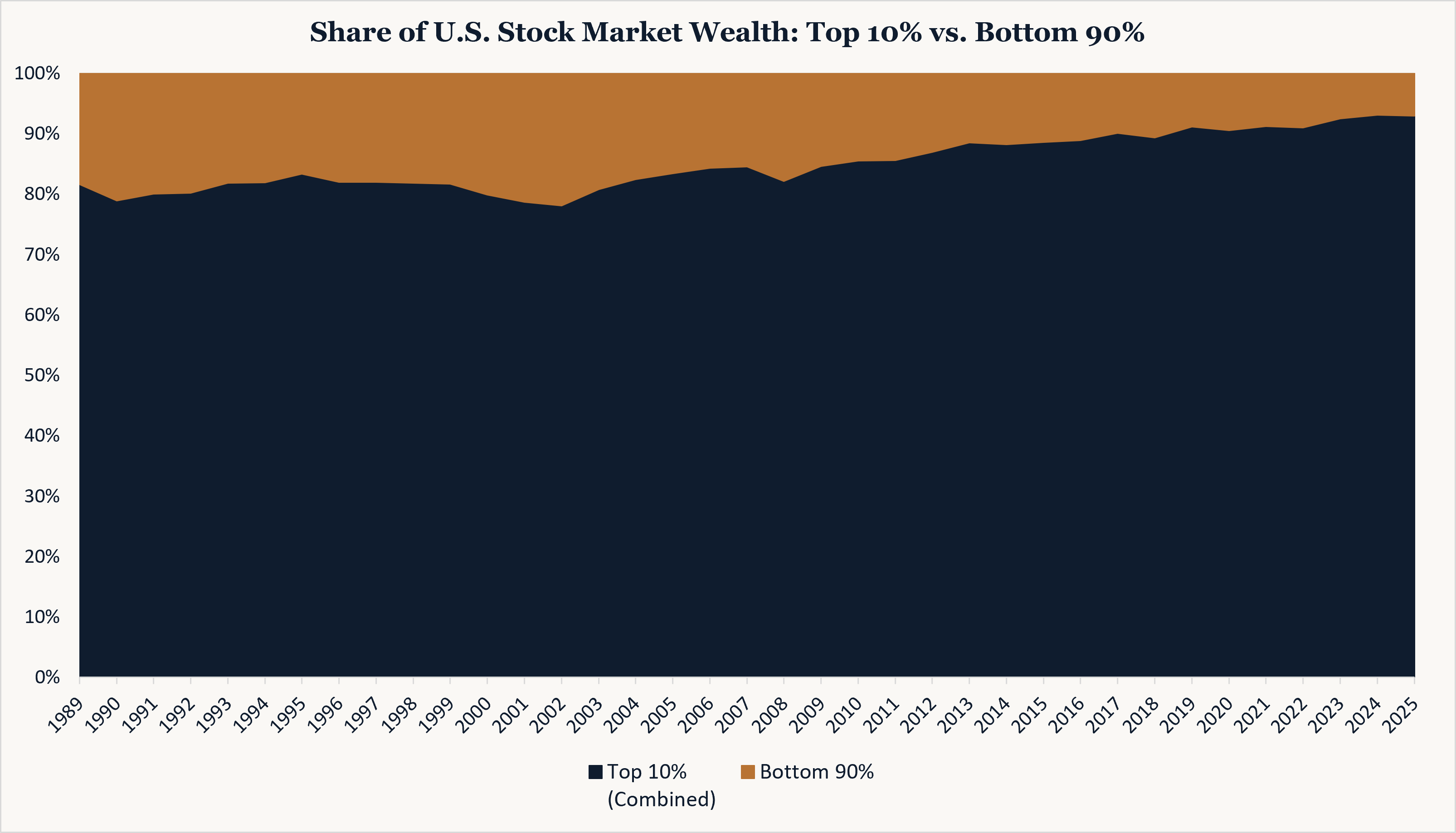

This is the wealth effect in action. The top 10% of households own 93% of the stock market. As equity values soar, their net worth expands, and they feel incredibly rich. They are the ones buying $40 half-chickens at Gigi's in Greenpoint, Brooklyn, and they do not care about the price. Their spending keeps the service sector hot and keeps economic growth positive, even as rising prices squeeze the bottom 90% of households to the bone.

This creates a brutal policy trap for the Federal Reserve. Cut rates, and the wealth-driven demand from the top 10% pours fuel on sticky services inflation: the $40 chicken gets more expensive, not less. Hike further, and you accelerate the credit deterioration already underway: auto delinquencies are running at post GFC highs, and higher borrowing costs would drive more fragile lower-income borrowers into default. Hold, and you watch the K-shape widen in real time. There is no clean exit. High car prices, soaring auto insurance premiums, and elevated interest rates have already turned car ownership into a luxury for the bottom 90%. The Fed's options are inflation, credit stress, or paralysis. Warsh faces this challenge. His honeymoon is likely to be short.

There is a debate on the stability of this economic split. The bull case is that high-income consumers drive almost half of all personal consumption in the United States. As long as tech and artificial intelligence earnings support the equity rally, their spending can carry the economy forward, allowing lower-income households to slowly catch up as real wages rise. The bear case is that the K-shape is inherently fragile. Rising auto loan defaults and credit card delinquencies will eventually bleed into corporate profits. If a stock market correction wipes out the wealth effect, the primary engine of spending stops, and the economy collapses.

So what do you do with a K-shaped economy where the Fed is trapped and the wealth effect is one correction away from reversing?

You stop reaching for yield where the credit stress is already visible. Auto loan defaults are the early warning. Credit card delinquencies are the next signal. High yield in consumer-facing sectors is the wrong place to reach right now.

Three places where the math still works...

First, private credit in senior secured asset-backed structures: equipment finance, litigation finance, and consumer receivables. The Fed's rate trap is your yield support here, not your enemy. Size these allocations to hold to maturity; liquidity assumptions break in a risk-off event. Second, real estate credit in logistics and data centers, shorter duration than equity, real cash flows. Third, in public markets, the opportunity is narrow but it is there: energy majors in the low-to-mid teens on forward earnings with yields north of 4%, and international developed markets at single-digit multiples with real earnings power. The S&P at today’s valuations is a return headwind, not a buy signal. Precision beats passive.

The most important uncertainty is the duration of the equity rally. If the stock market corrects meaningfully (think 20%), the top 10% will freeze spending, and the illusion of economic growth will vanish. The $40 chicken is keeping the lights on. But the nearly 13-year-old car is the real story for most of America.

IMPORTANT DISCLOSURES

Zidle Macro Strategy Group is an independent macroeconomic research and commentary service. The content in this publication is informational and analytical in nature and does not constitute investment advice, a solicitation, or an offer to buy or sell any security or investment product. ZidleMSG is not a registered investment adviser, broker-dealer, or fiduciary under any federal or state securities law.

This publication does not recommend, endorse, or make any specific buy, sell, or hold recommendation for any security, ETF, mutual fund, private fund, or other investment vehicle. Any companies, individuals, or projects referenced are discussed solely for analytical and illustrative purposes. ZidleMSG has no financial relationship with, and receives no compensation from, any entity mentioned in this publication.

All commentary represents the views of the author based on publicly available information and macroeconomic analysis. Such views are subject to change without notice. Past commentary does not constitute a performance track record, and no representation is made that any analysis or forward-looking view will prove accurate.

Investing involves risk, including the possible loss of principal. Readers should conduct their own independent research and consult a qualified financial, legal, or tax professional before making any investment decision. ZidleMSG assumes no liability for any investment decisions made in reliance on this content.

© Zidle Macro Strategy Group. All rights reserved. Reproduction or redistribution of this content, in whole or in part, is prohibited without the prior written permission of ZidleMSG.