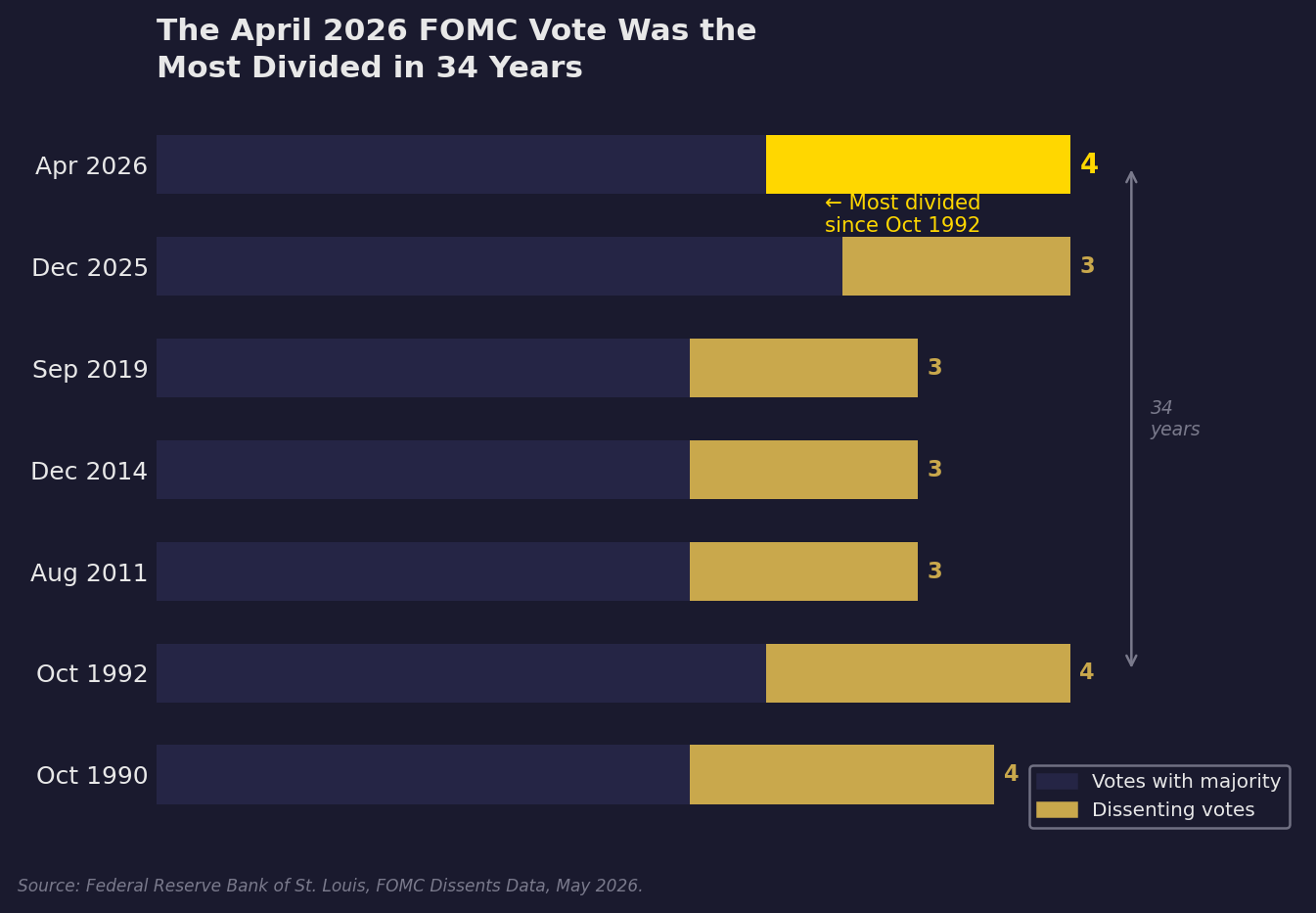

Incoming Fed Chair Kevin Warsh may want to begin with patience. The harder question is whether the Federal Reserve he inherits will allow it. According to the data, the April 2026 vote was 8-4, the most divided policy vote since 1992. Three officials objected to retaining an easing bias, while one wanted a 25 bps cut. That is not a routine split. It is a warning that the Committee's center of gravity is already moving away from automatic cuts.

Warsh's first problem is that patience now has to be earned. The effective fed funds rate was 3.64% in April. Unemployment was 4.3%. Headline CPI was up 3.8% year over year in April, and the PCE price index was up 3.5% year over year in March. Those numbers do not prove the Fed must hike tomorrow. They do prove that a cutting bias is hard to defend without a clearer disinflation story.

That is where history matters. Specifically, the 1996 Greenspan Fed. Greenspan also faced a technology story before the data had fully caught up. His contacts in the tech industry were telling him the internet was transforming productivity. The measured data did not confirm it. He chose to believe the narrative anyway. His argument was not that inflation risk had disappeared. It was that technology, measurement problems, and delayed productivity gains might be changing the economy's speed limit, so the Fed should not tighten preemptively on old assumptions. That patience worked because inflation stayed contained, and because Greenspan had accumulated the institutional credibility to persuade the Committee that forbearance was not complacency.